A bill called the Swaps Regulatory Improvement Act recently sailed through the House Financial Services Committee. But when The New York Times went through emails from a lobbyist to the congressmen who wrote it, the paper discovered an unofficial co-author: Citigroup.

It turns out that recommendations from Citigroup made up 70 of the bill's 85 lines, with two important paragraphs copied almost verbatim — save for two words that were changed to make them plural, according to the Times.

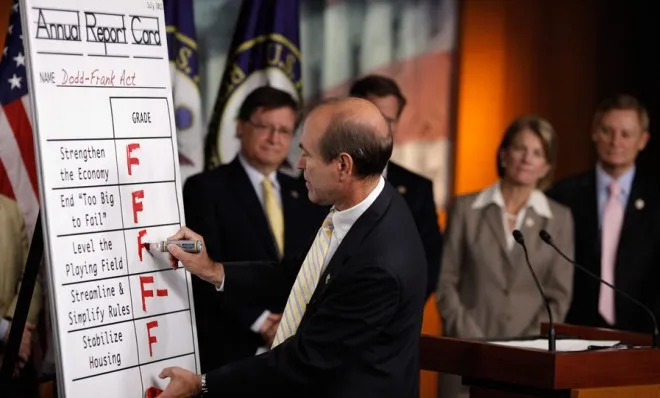

The bill takes aim at the 2010 Dodd-Frank Act, the financial regulatory reform bill that was meant to prevent a repetition of the 2008 financial crisis. The specific provision in question forbids banks from trading certain derivatives that critics say were instrumental in causing the crisis. Under Dodd-Frank, those derivatives would have to be moved to affiliates that weren't FDIC-insured, lessening the chance they would be the recipients of government bailouts.

The Week

Escape your echo chamber. Get the facts behind the news, plus analysis from multiple perspectives.

SUBSCRIBE & SAVE

Sign up for The Week's Free Newsletters

From our morning news briefing to a weekly Good News Newsletter, get the best of The Week delivered directly to your inbox.

From our morning news briefing to a weekly Good News Newsletter, get the best of The Week delivered directly to your inbox.

Latest Videos FromThe Week

Erika Eichelberger at Mother Jones also compared the Citigroup draft of the bill with the final House version and found them "practically identical." She noted that Citigroup has long played a role in relaxing financial regulations, including the 1999 repeal of the Glass-Steagall Act, which once prevented commercial banks from engaging in the same activities as investment brokerages.

Citigroup was the "bank that administered the coup de grace to Glass-Steagall," Marcus Stanley, policy director at Americans for Financial Reform, told Mother Jones.

Citigroup defended its lobbying efforts in a blog post on its website. Ed Skyler, head of global public affairs, wrote that the provision "does absolutely nothing to create a safer financial system." Instead, he wrote, it would "create undue costs and burdens on U.S. financial firms," which will force them to "simply do business elsewhere."

Skyler also noted that the bill was bipartisan, which is true. The majority of congressmen who supported the legislation were Republicans, but it was co-sponsored by Rep. Sean Patrick Maloney (D-N.Y.), who, the Times reported, recently held a fundraiser in Washington, D.C., in which corporate executives and lobbyists paid up to $2,500 to have dinner with him.

While there has been a notable lack of bipartisanship in Congress in recent years, it appears that both Democrats and Republicans are more than open to Wall Street's money. As Sen. Dick Durbin (D-Ill.) once said of Congress, banks "frankly own the place."

"Democrats can’t be trusted to control Wall Street," Robert Reich, former secretary of labor under President Clinton, said at Salon. "If there were ever an issue ripe for a third party, the Street would be it."

Even those who supported the bill said the close relationship between the banks and lawmakers was unseemly.

"It’s appalling, it’s disgusting, it’s wasteful and it opens the possibility of conflicts of interest and corruption," Rep. Jim Himes (D-Conn.), a former Goldman Sachs banker and member of the House Financial Services Committee who backed the bill, told the Times. "It’s unfortunately the world we live in."