We need to send people money. We need to fix how they get it, too.

Putting the coronavirus stimulus into action will be much harder than it should be

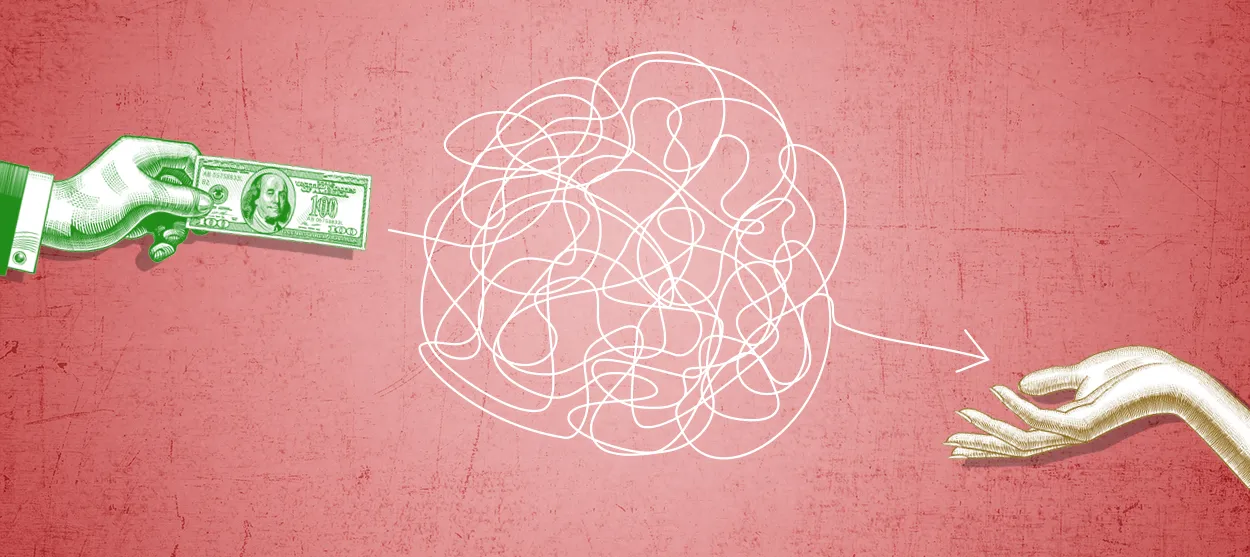

To battle the economic crash from the coronavirus pandemic, Congress is sending Americans cash. The deal just hammered out will send $1,200 to every adult making under a certain income threshold, and $500 for every child. But will the money actually get to everyone?

In many cases, it turns out, it could take weeks or months. And many of the poorest and most vulnerable Americans will face further difficulties once the check arrives.

"The Treasury Department is expected to begin directly depositing checks within a few weeks of the bill's passing," The New York Times reported. "But mailed payments will take one or two weeks longer, Republican Senate aides said Wednesday." It sounds like the mailed checks, for individuals who don't have bank information already on file with the IRS, could take up to two months, and earlier reports suggested they could take up to four. And that time frame doesn't even get to the question of people who may be too poor to have filed taxes, who may move a lot, or who may not have reliable housing, and whose address has to be pieced together from Social Security data or the Veterans Administration.

The Week

Escape your echo chamber. Get the facts behind the news, plus analysis from multiple perspectives.

Sign up for The Week's Free Newsletters

From our morning news briefing to a weekly Good News Newsletter, get the best of The Week delivered directly to your inbox.

From our morning news briefing to a weekly Good News Newsletter, get the best of The Week delivered directly to your inbox.

Meanwhile, one out of every four U.S. households either has no bank account or has real trouble accessing one, which adds further hurdles to actually being able to use the money. "You'll have to cash that check, and take that cash and put it into a money order again to pay your bills," Mehrsa Baradaran, a professor at the University of California at Irvine who studies banking inclusion and inequality, told The Week. That process will impose further fees, not to mention the costs, time, and effort required to physically go from the check casher to the utility and landlord's offices to pay bills and rent.

Senate Democrats, including Sen. Sherrod Brown's office, tried to do something about this. Baradaran helped Brown draft a provision that would give any American who needed it a free banking account — available at any local bank or post office — in which the $1,200 aid could be directly dropped. Others in the House, like Rep. Rashida Tlaib (D-Mich.), have their own proposals to do something similar. Ultimately, none of this made it into the Senate deal, which has now passed the House and is headed to President Trump for signing. But Brown and Tlaib have also introduced their proposals as standalone bills. And we really need to fix this, for both moral and economic reasons.

Around 8.4 million U.S. households (or 6.5 percent) are "unbanked," meaning they have no bank account at all. Another 24.2 million households (18.7 percent) are "underbanked," meaning they technically have a bank account but have real difficulty using it. As Baradaran explained, low-income Americans' finances don't mesh well with banks' business models, which are designed more for the steady income flows of the middle class. Less fortunate Americans are constantly hit with fees for things like overdrafts or not having enough money in their accounts. Nor are they particularly profitable for banks, so many institutions have simply abandoned those communities, leaving people with either no banking option, or a branch that's 50 miles away. Regulations used to require banks to keep a branch in every community, but those rules were dismantled in the 1990s, and "those voids were filled with payday lenders and check cashers" as Baradaran put it. Those outfits charge even more onerous fees and interest rates for their services.

Imagine the U.S. payments system as three concentric networks, with each network serving different groups — and each of very different quality. The innermost circle links the Treasury Department and the Federal Reserve with the major private banks, and those banks to each other. This network can settle transactions extremely fast, say three to five days. (There are efforts afoot to get this down to 24 hours or less.)

Join 350,000+ subscribers and keep yourself informed with a selection of The Week’s most interesting, enlightening and entertaining stories - plus daily puzzles.

The next network out is essentially the public-facing side of the private banking system — it's what connects individuals and households and businesses to the banks. This is the network that can get everyone their direct deposits in a few weeks.

This situation is already rather remarkable, since we have a public system — the first innermost network — that no one but big private banks are allowed to participate in. Meanwhile, private for-profit banks get the privilege of being the middle-man between that public system and the actual public. "There's no reason banks should be that middle man unless they're mandated to give everyone an account, and they're not," Baradaran noted.

Things are even worse out at the fringes of the circles of inclusion. That's the third network that serves the unbanked and the underbanked and people less directly tied into the second network. This is where people have to wait two months for a check in the mail, cash it with a bank if they're lucky, and otherwise go through the whole obstacle course of check cashers and payday lenders and money orders.

At a minimum, we should plug the people in the third fringe network directly into the first, which is what Brown's bill would do. Under that proposal, when your check got mailed to you, you could pick it up at the post office and open a simple banking account — free, no fees, no minimums — that would plug you directly into the Fed and Treasury Department's payment system. You could cash your check right there and use the money via a debit card that would come with the account, without dealing with any profit-seeking third parties.

Providing a public option for basic banking services via the U.S. Postal Service is an idea that's actually been floating around for a while — in fact America did do that, from 1911 to 1966. (There are also proposals to just give every American an account with the Federal Reserve directly.) Baradaran said her "dream version would be every post office would have this option" — i.e. use this scheme to take every American in both the second and third networks, and plug them directly into the first, innermost network. But Brown's more limited bill would've at least plugged the third network's unbanked and underbanked into that first inner network.

Admittedly, this wouldn't completely solve the initial problem of how fast the checks go out. But it would help, and it would end the obstacles and exploitation that marginalized Americans face when using the money. And if Congress needs to authorize more of these payments — which will almost certainly be needed — the bank accounts will now be in place.

Tlaib's bill is even more ambitious: It would give every American a pre-paid debit card that would plug directly into that inner network, and that Congress and the Treasury Department could automatically refill with money whenever they wanted. In fact, Tlaib's proposal called for every individual of all ages to get an initial $2,000, followed up by monthly installments of $1,000 until a year after the crisis is over. "It's trying to provide a novel infrastructure through the pre-paid cards, to get past the limitations of direct deposit or mailing checks," Rohan Grey, president of the Modern Money Network, who helped Tlaib's office draft the proposal, told The Week. (News reports tended to ignore this aspect of Tlaib's bill, focusing instead on its unusual financing mechanism: have the Treasury Department mint trillion-dollar coins and deposit them with the Fed to avoid having to issue new debt.)

The U.S. government already uses similar debit card systems for programs like food stamps, so the basic infrastructure is in place. Between mailing the cards and making them available for distribution at banks and post offices and schools and the like, Tlaib's proposal might actually have been able to get the first payment out even faster. And again, further payments would be automatic, and the debit card system could be integrated with a postal banking public option or Fed-accounts-for-all down the line.

Unfortunately, as I mentioned, none of these ideas made it into the final package. It's not clear why, but we can speculate: lobbyists for industries like payday lenders have clout on Capitol Hill, and these proposals would be an existential threat to their industry. For the moment, the ease and reliability of that inner network remains a privilege reserved for the powers of the banking and financial industries, while we mere citizens have to deal with the private banking system on its terms — and the least fortunate among us are left out in the cold entirely.

Many of the millions who have already lost jobs probably need money now. Even people who still have jobs, but who don't earn much, face a coming cascade of hardships, from the need for food, rent, utility bills, and more. (The government also didn't do itself any favors by making the money means-tested, which will add further time for government agencies to calculate what everyone is owed.) Millions of human beings will suffer because of the delay. Meanwhile, the longer it takes for that money to hit people's pocketbooks, the more time there is for the negative feedback loop of job loss leading to less spending leading to business closures leading to more job loss to build on itself, deepening the hole the economy will eventually have to dig out of.

But Congress can always pass more bills, and by all accounts the coronavirus crisis will last long enough that political pressure for more cash aid to average Americans will likely become overwhelming. The sooner we can stand up a fast and simple public banking option for all, the faster we can get aid out to everyone — both in this crisis and the next.

Editor's note: A previous version of this essay misstated how much money individuals would receive under Tlaib's plan. It has been corrected. We regret the error.

Want more essential commentary and analysis like this delivered straight to your inbox? Sign up for The Week's "Today's best articles" newsletter here.

Jeff Spross was the economics and business correspondent at TheWeek.com. He was previously a reporter at ThinkProgress.